Today was a typical day in the crazy menagerie of our home. But it was delightful. I’ve come to accept that Saturdays are overscheduled and hectic. Sundays are a rest day.

F. Bean Barker woke at 5:30 am— a normal part of the routine in her old home. No one gets up that early here.

I went to bed around 2:30 am so when Ms. Black Bean woke up and barked/whined/howled for 30 minutes, I texted teenager #1. She went down, covered the dog’s crate with a blanket and laid down on the couch beside the dog to go back to sleep.

After that 45-minute disturbance, I woke at 9:30 am. The teenagers finished picking up the house to prepare for the notary arriving at 1 pm.

We cared for our pets and crated Vesta and Minerva of the FURR Roman Pride for the adoption event at Petsmart.

We then stopped at Dunkin on the way home because I wanted to do something to thank my husband for taking the time to come sign this paperwork and for supporting me in the refinancing of the house. It’s been about 20 months since he’s lived here with me. Neither one of us has filed for divorce. So his name is still on the deed of the house and the current mortgage.

This new mortgage will pay off my car, save me $300 a month, though also extend my term five years. Now instead of the house being paid off by the time I am 55, I will be 60. Mortgage payment alone on the the refinancing will pay off is 50% of my take-home monthly income and that makes me nervous.

My hope is that once the pandemic ends and life shifts, new opportunities and stability will allow me to apply extra money to the principal.

And teenager #1 will take her drivers exam Tuesday. If she passes, her dad and I will have a massive insurance bill so my solace is that if something should happen to my car, at least it is paid for.

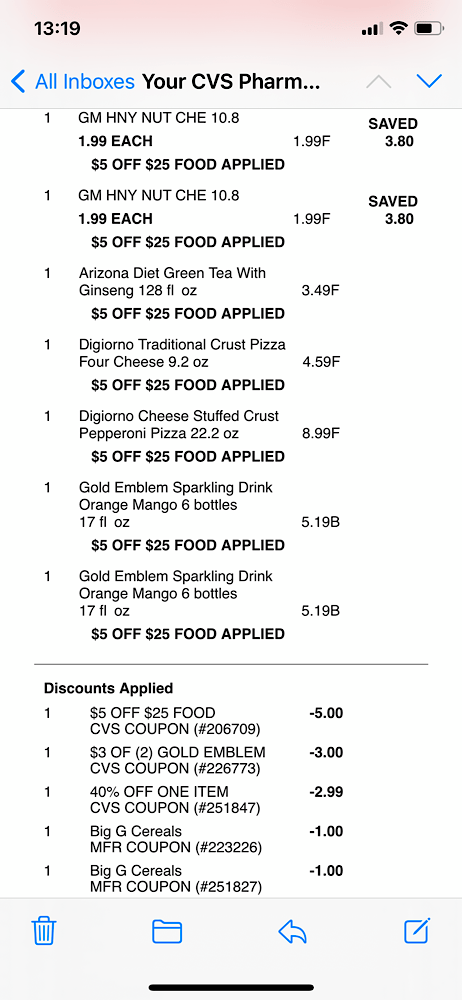

Teenager’s dad loved his new cold foam chocolate stout cold brew. The closing almost went without a hitch, but Fog decided to saunter across the table amid the notary’s pile of papers. Cats are not allowed on the table. Especially when we have guests.

The teenager got ready for work and we watched an episode of Canine Intervention on Netflix. I wish they had more episodes.

I dropped her off at Tic Toc Diner. I then went to get the kittens.

Those adorable tuxedo sisters then went to Petco (Greenwich Township, NJ) for their adoption habitat.

Vesta, having spent about three weeks in the habitat at the other Petco, sat there and shook in fear.

I came home planning to walk F. Bean Barker with our neighbors, Jan and her Ladyship Sobaka. But Bean only made it a half-block.

She’s just exhausted.

And then Jan and I went to pick up Nan and have dinner at Tic Toc. The teenager was worried about not having a Braille menu for Nan. As if we need a menu.

The teenager told me the founder stuffed with crab looked really good as the cook took a lot of care in its preparation and plating. I ordered it. With coleslaw. And the silly waitress got me french fries instead.

The dish reminded me of a crab cake wrapped in other fish. So good and a ridiculous amount of food for the price.

After dinner, Nan and I hung out at my house until it was time to retrieve our waitress from the diner.

And then when she got home, she unboxed this month’s box from Witch’s Gifts. These items are so carefully curated. To see the unboxing: March Box Witch’s Gifts

These boxes (and my tarot and witchy podcasts) remind me that I need to pay more attention to my spiritual and magical development.