I keep promising myself that I won’t let this blog anguish and fade into nothing, and then I fail. If you miss me, check out Parisian Phoenix Publishing on the web or social media or sign up for my weekly-ish Substack newsletter. (Which you can do here.)

While I keep intending to do more jovial hometown adventures and life updates about the cats, the bird or the dog, it doesn’t happen. (We have TWO dogs this week as we have a jovial mutt with us as a boarding client. He’s a joy to be around, and he’s such a confident and stereotypical dog compared to our depression-prone backyard-bred pit mix.)

Eva’s dog has received a custom muzzle as a safeguard against her fear-based reactivity. And the difference it makes in our ability to trust her with new dogs and people and her comfort while wearing it is amazing. If you have a dog with issues, a custom muzzle is a game-changer.

But today I want to talk about what happened when I returned from Ireland regarding my emergency room visit two months prior. And I might sound like a conspiracy theorist, but it is what it is.

I have a high-deductible, employer-sponspored health plan through my husband, but as we are separated, I do not ask him to use his HSA. The HSA absorbs a lot of those out-of-pocket expenses. And my husband’s employer gives him money for the HSA as an incentive to take the high-deductible plan.

I have done the math. As a family, we have had the high-deductible PPO plan for 20 years. It sounds scary at first, but the monthly premiums are way cheaper than the other plans and the PPO allows us to see any doctor we want when we want, and when you have chronic issues, that’s important. I briefly had an HMO in the late 1990s when I had never had any health insurance before and no real medical treatment post age five, and my primary care doctor sent me to a podiatrist who specialized in ankles for my gait issues because he was pretty much the only provider in network. He told me there was nothing anyone could do without finding a provider in a major city.

And by the way, he was wrong.

If you don’t know, a high-deductible plan means that the insurance company pays nothing of any of your expenses until the deductible is met. In my case, that’s $3,500. BUT, my out-of-pocket maximum is $5,000 a year.

The ER Bills

As you may recall, (if not here it is: the original post and the ortho follow-up) in early January I had a fall and I debated between going to the ER or the urgent care because of my history with afib after bodily trauma… I was not in afib, but I did break my thumb, which has not fully recovered.

That fall led to about $800 in out-of-pocket orthopedic specialist bills and about $3,000 for the emergency room. Now, I use AblePay which allowed me to schedule payments for these services and gain a cash discount. For the ER bill, I opted to pay more than $2,000 in one lump sum of my American Express because it allowed me the largest discount. I then used the AmEx PlanIt feature to schedule that into monthly payments for a fee instead of accruing interest. In the end, I didn’t save money but it allowed me to space the payments.

But then… randomly, a full month after I paid 100% of the ER bill in a lump sum of on my credit card, my insurance company (Capital Blue Cross) decided to renegotiate the bill– which remember, they did not pay. I did.

I did not know this was happening. I was less than $200 away from my out-of-pocket maximum for the year so I scheduled regular chiropractor appointments and a mental health check-in with my therapist. The chiropractor appointments help me not twist my body into weird contortions that further cause complications from my irregular gait, and since my chiropractor Nicole was originally a physical therapist, she helps me stretch and monitors my gait to make sure my feet “do feet things.”

So, while I have debt from the ER visit, I can now have chiropractor appointments every other week for a small coinsurance amount ($40). And that is a huge help to my mobility.

On a Friday afternoon, I get an email from AblePay and a notification from AmEx that I had a $1700 refund on my recent medical bill. Which sounds great, right?

I logged onto Capital Blue to see what was going on, and indeed they had renegotiated my bill, which rolled back my previously met deductible and out-of-pocket maximum. And I had two chiropractor appointments and two therapist appointments that I was now responsible for. That’s about $700.

And I know what you are thinking, that still leaves me $1,000 ahead. But oh no it does not. Because remember, I had only paid one payment of my planned credit card charge. So the whole refund went to the charge, and I still needed to pay the remaining several hundred.

I negotiated a payment plan with my therapist and canceled all my upcoming chiropractor appointments.

I wish I could tell you that was where the story ends.

Present Day Repercussions

When I was in Ireland, I walked a lot more than usual. A lot more. As it was a relatively last-minute trip, I didn’t have a chance to try and get myself in shape. So I attributed the discomfort to my out-of-shape-ed-ness and called it a day.

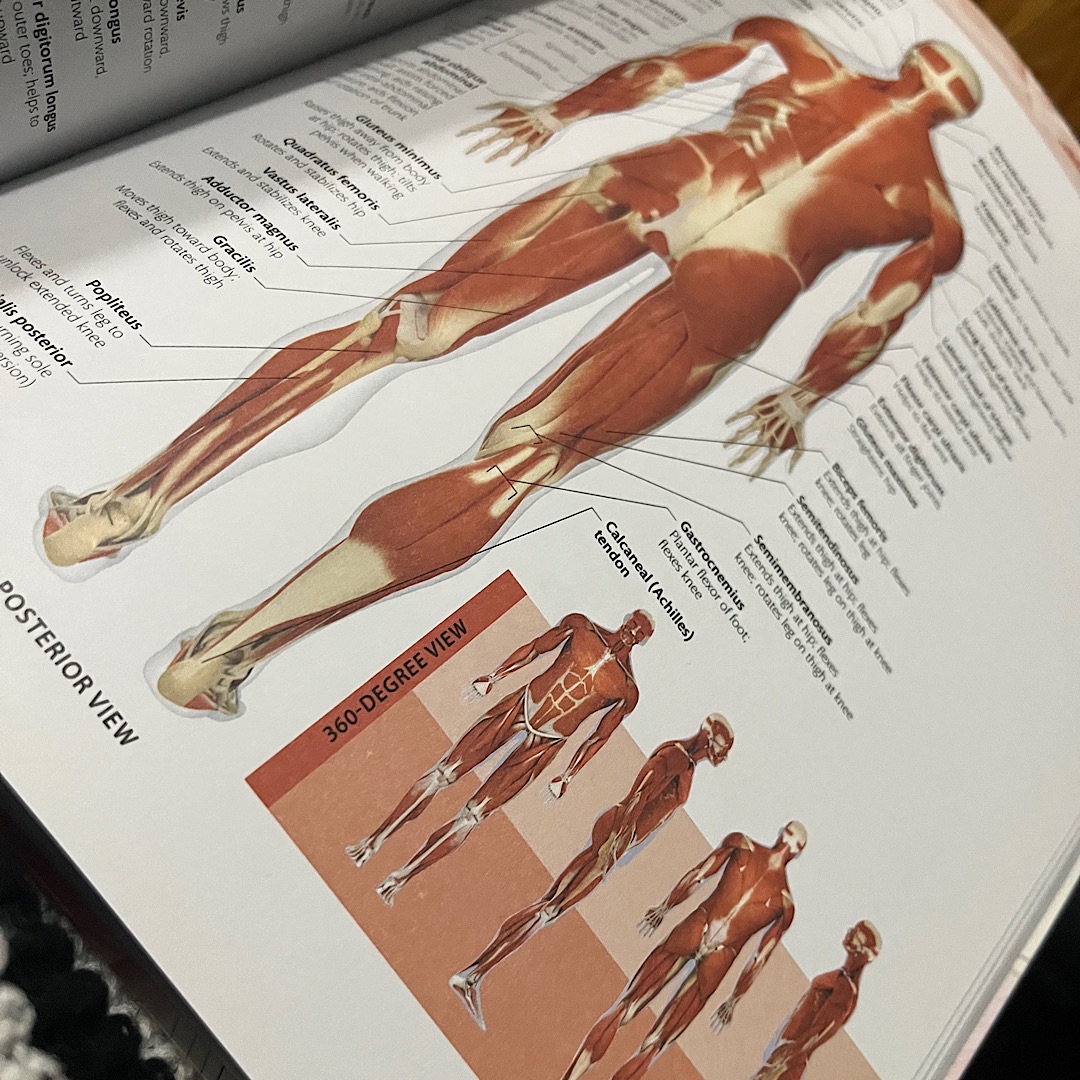

But I am experiencing problems again. For the last week, I have been experiencing increased muscle pain in both my legs. My left leg usually does not hurt. My right leg always hurts. Like every day, I experience at least a pain level one but typically two or three. It’s like there is a braid of muscle that splits the back of my thigh muscle and presents with a constant pulsing, ache. But increasingly, my calves are experiencing extreme, painful muscle stiffness, in both legs, and my knees hurt.

My flexibility is better than usual, and I have no problems with my back, but if I touch the floor, it kills me to straighten my legs.

And this morning, after a week or so of this, and several days of feeling like my legs aren’t attached to my body when I walk, I started to cry. I caught myself, but I still started to cry. I took an extra dose of my baclofen– at double strength, and that made the calf pain go away. But I’m struggling to use my legs. And I’m getting damn tired of it.

I have tried to find and label what muscle hurts, but I can’t.

I suspect I need physical therapy. I have tried to take short but regular walks, making sure that I hit at least 5,000 steps daily, but I think it’s too little too late, and my muscles have forgotten how motion works. This winter was hard, long and cold; and with my part-time fast food job laying me off, I don’t stand and walk as much as I have during the last year.

But that leg pain I refer to as a braid? That started shortly after Stitch Fix closed. I think because I went from a job where I stood eight hours a day to a sedentary job. That’s almost three years of the same pain. That has now intensified.

So, why don’t I call the neurologist?

Because she costs $220.

And if she wants tests, I can’t afford those.

And If she agrees that I need physical therapy to stretch out and retrain muscles, that’s thousands of dollars. It sounds ridiculous. That a six-week physical therapy session would rack of thousands of dollars, but when I broke my ankle, which was TEN years ago, that cost me $5,500. That deductible and co-insurance adds up.

This is when I miss my Medicaid.

Becuase I work hard, everyday, and I just can’t afford the treatment and maintenance that would improve my quality of life.

And it sucks.

To make a choice everyday to deny yourself care you need.

Because of money.

And I believe– and maybe I’m wrong– that Capital One renegotiated my ER bill because I hit that out-of-pocket maximum and they didn’t want to pay my upcoming bills.

Our health care system, specifically for-profit, employer-sponsored health insurance, sucks.

It’s broken.