It’s approaching 1 a.m. and I am amazed at how quickly I am adapting to going to bed around 1:15 a.m. and waking up around 8:45 a.m.

An hour ago I was placing my laptop into the cupboard, taking my last cart of fixes to the “garage” area and heading to the time clock.

I only walked 16,000 steps in the warehouse tonight but I hit the pre-direct pick picking goal of 128 fixes.

I am sitting in my bed with a gin-and-cucumber-positive-beverage-B12 cocktail. I have kittens surrounding me (the Norse Pride domestic long hairs) and Nala chattering and falling asleep on my knee—and I know my bird should be asleep right now but she wakes up when she hears me come home and she’ll be super angry with me tomorrow if I don’t give her a bedtime cuddle.

She just fell asleep — on my knee.

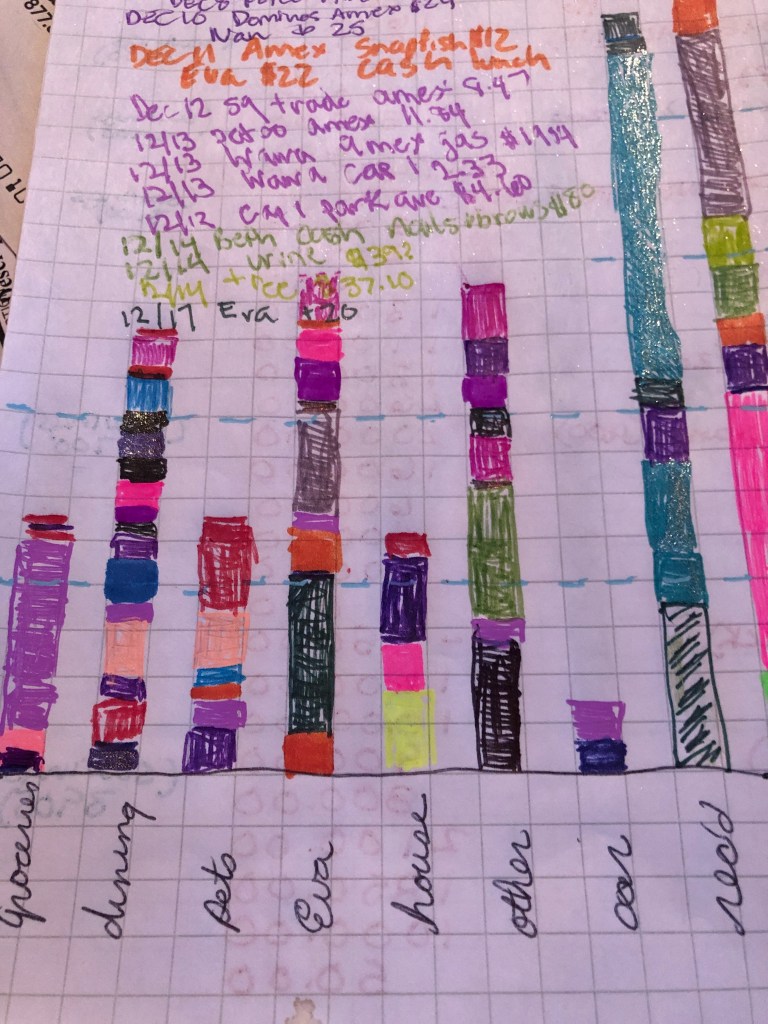

The scene looks something like this:

Poor Fog is whimpering outside my door as he used to be the cat that slept with me until the teenager moved the Norse Pride (some of our foster kittens through Feline Urban Rescue and Rehab) into my room. He wants no part of those pesky furball kittens.

But he misses me now that I am working, and he pursues every opportunity he can to be with me.

Today involved some meetings, including the Lehigh Valley Regional Homelessness Advisory Board. I organized some paperwork and paid some bills as this week’s unemployment payment came.

I received EBT/SNAP (food stamps) for September, October and November so I’ve been combing every store possible for the best deals. Grocery Outlet and Lidl remain my standbys, but I find some good coupons at CVS. Today they sent me a coupon for a Starbucks Frappuccino from their ready-to-drink cooler for $1.49. I had $1 in Extra Bucks expiring today so I got the coffee beverage for 49 cents in food stamps.

Why does SNAP pay for candy and bottles of Frappuccino but there is no program to pay for bath soap, laundry supplies or toilet paper? One friend remarked that poor people must not be allowed to be clean.

So, now that I’m employed again these are issues I shouldn’t have to contemplate much longer.

And I suppose eventually StitchFix might ask me to stop blogging about them but I hope not— I’m a wholesome blogger with a long history in the public relations and journalism field.

But I’m so excited about hitting the 128 number and we had Thanksgiving dinner at work!

Thanksgiving dinner served with Covid protection

Picking Goals

Hangers

My end of day totals