For the first 15 years or so of our marriage, I used Quicken to do our household finances. We have always been one of those households just making ends meet, sometimes saving up, only to have something happen to suck our savings away.

When Quicken went to a subscription based cloud product, I groaned but paid the piper because I had almost two decades of financial records in that software.

And then, in late 2018, my 2013 MacBook Air died.

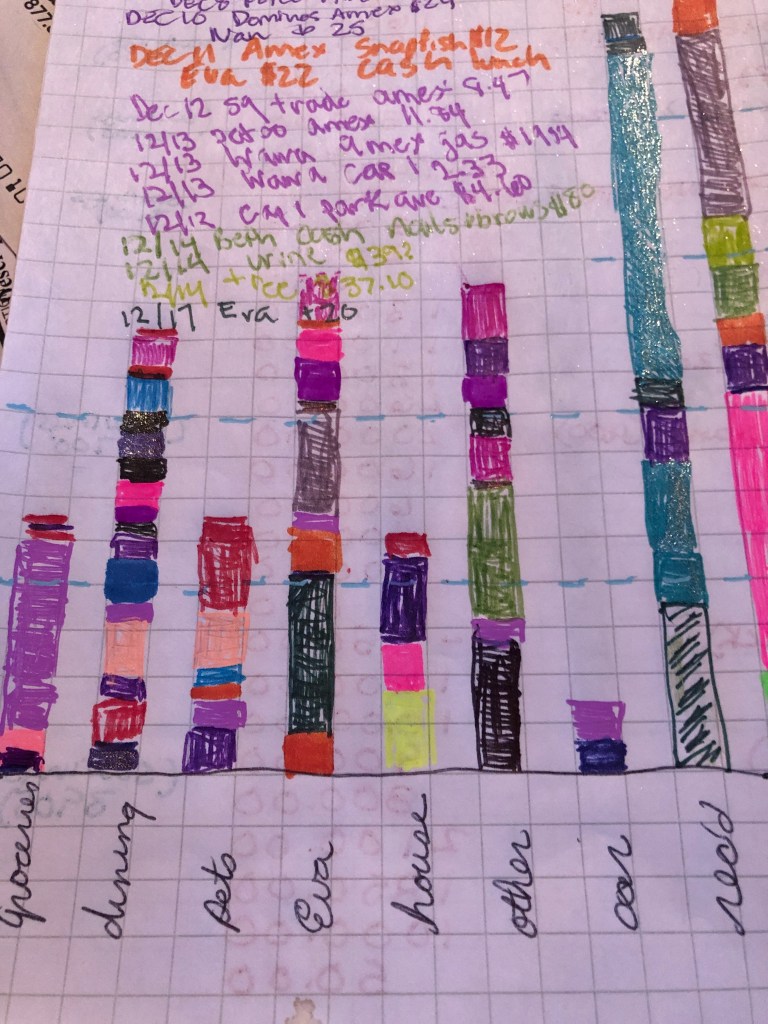

I developed a system to keep my finances organized—

using graph paper.

Each square is $25 in expenses I spent in a month not part of the regular cycle of bills (mortgage, car payment, electric, fuel oil for heat, water, sewer/garbage, car insurance). That is just so I know where my moment went for future planning.

I keep one column for “cash” and one for “credit” above the graph to detail the spending.

95% of my credit expenses go on my American Express, and I keep a Discover in my wallet for those places that don’t take American Express. I typically pay off my entire balance each month (which is where all that tallying and calculating what I’ve spent comes in handy) but recently I used a free trial of American Express’s “plan it” feature to pay some medical bills and for Nala, my Goffin’s cockatoo.

I keep a sloppy register of my checks also in the budget book, and I compare balances against my budget for the month or quarter at least once a week.

But here’s my big hack. I am known to take my credit cards out of my wallet and I never carry my ATM card.

Yes, you heard me.

I don’t carry my ATM card in my wallet. I keep it in a drawer at home. If I want to extract money out of my bank, I have to plan it. Or run to Target and use my Target debit card. This keeps those little expenses from adding up.

There is no “let’s run out and get a sandwich.” That kind of thing.

But, you say, what if something unexpected happens? Well, I do have what I call my discretionary spending card.

I have a Capital One online account where I put whatever money I think I can spare after I pay the bills. Honestly, that’s usually the grocery money. Right now there is $12 left in that account. No, make that $8. I forgot I stopped at DQ for Buy One Get One for 80 cents Blizzards. That is the ATM card I keep in my wallet.

If I get impulsive, if I drop it, if it gets stolen, if it gets hacked… it’s not the account I use to pay my bills.

Plus, I have a savings account in Capital One, so if I get really stuck, I can transfer money between those accounts on my phone. And money between my main accounts and my Capital One accounts also takes a few business days, so it does require planning.

But I’m good at planning.

So right now I’m going to update the budget as I had some more large bills come in (dental crown $400 out of pocket; furnace maintenance agreement $250) plus car insurance is due in two weeks.

I pay for six months at a time and it’s due on the same day as the mortgage.

Speaking of mortgage, when we were 12 years into our 30-year-mortgage I refinanced the house from 5.5% down to 3.25% in a 15-year loan. Too many people want to lower their monthly payment, whereas I focused on shortening the term on the loan.

I borrowed enough money to pay off the car and some credit card bills (an unexpected household repair and my daughter’s euphonium had us in for about $5,000) AND cut two years off our original mortgage length for the same payment as our original mortgage but we were saving an additional $300/month not having a car payment.

I also had them add an additional $50/month for principal curtailment to my mortgage payment. So if I ever need to I can have the mortgage company drop that and I can have a lower mortgage. In the meantime, my principal is dropping.

I do something similar with my car—once I calculate my budget for the quarter I pay anywhere from $50 to $200 extra on my car payment. I think I financed $15,000 less than 18 months ago and already my pay off balance is about $9,000.

My other tip is to have an automatic transfer into a savings account. Most banks encourage this and will waive fees and offer overdraft protection if you do it. I transfer $200 a month into my savings account and sometimes I have to transfer it back to checking the next day. Normally I can live without it, and when a shortfall happens I have that back-up.

Budgeting and financial planning when you’re in a low-to-moderate income household is hard. It’s a puzzle. Knowing what it takes to run your household is key. Planning is a must.

PS— yes that is my credit score

2 thoughts on “Budgeting”